So-Called Fact Checkers Keep Butchering The Facts About Obamacare

All the Pinocchios.

Since its passage, and in a way that is unlike any policy issue in modern American history, the press have rallied to the defense of Obamacare. From day one, there has been almost no light between the average liberal activist and average health-care reporter.

Or the average “fact checker,” for that matter. “Fact checking” has evolved from an occasionally useful medium to an exercise in revisionism and diversion. Take The Washington Post writer Glenn Kessler’s recent article titled “President Trump’s mangled ‘facts’ about Obamacare.” Headline readers might assume it’s just Trump doing what Trump does most of the time. I almost passed myself. Yet it turns out that all these supposedly “mangled” contentions about Obamacare are, at the very least, debatable assertions.

Kessler, for example, doesn’t approve of this Donald Trump statement: “Americans were told that premiums would go down by $2,500 per year. And instead, their premiums went up to levels that nobody thought even possible.” Other than the hyperbole (“nobody thought even possible”), this statement is substantively true.

Kessler’s ostensive debunking of the “premiums are soaring” claim is really just a confirmation that premiums have indeed risen, augmented by an argument that it wasn’t Obamacare’s fault. Kessler blames the vagaries of modern life and demographics—because these things apparently didn’t exist when Democrats were making their big unrealistic promises in 2009.

More interestingly, Kessler contends that when the former president promised Americans that their insurance premiums would drop by $2,500 for an average family, what he really meant was premiums would be $2,500 less than the anticipated rise. So in other words, according to estimates the average family is now supposedly paying $3,600 less than what they would have paid if Obamacare hadn’t been passed.

Two things: One, as we will see, Kessler (and many others) won’t accept this context when Republicans correctly use it to talk about supposed Medicaid “cuts.” Second, it’s simply not true. Obama repeatedly stated — probably hundreds of times over a two-year span — that the bill would “reduce” the cost of premiums by $2,500 for the average family. Perhaps it exists, but I can’t find a single instance anywhere of President Obama, or anyone selling the legislation, offering a nuanced context about reductions in the rise of premiums in relation to a baseline.

Despite Kessler’s efforts at creating this equivalence, Republicans who bother to defend their potential Obamacare repeal bills are pretty explicit in explaining that Medicaid “cuts” merely slow growth in spending. So, at the very least, the former president was purposefully misleading the American people.

But according to Kessler, Obama didn’t lie or “mangle facts” or mislead anyone. Rather he gave a “misguided … pledge.” The word “misguided” intimates that Obama wasn’t misleading anyone on purpose. In another apologia on the issue, Kessler writes that “Obama was less than clear with his wording, and the Republicans took the former president’s claim at face value.” Oh, did they? The promise of lower premiums, coupled with the lie that you could keep your insurance if you liked it, were the central political selling points of ACA to the middle class. They were the only aspects of the law that would have benefited those who already had health insurance.

Moreover, Kessler does not use this generous standard to rank Republican statements about Obamacare. Obama was given two Pinocchios for making a patently false “pledge” on premiums,” and Trump was given three for pointing it out. (Update: this mark was given by Kessler’s predecessor, Michael Dobbs. So it is unfair to make the comparison.)

Kessler also doesn’t approve of Trump saying: “Insurers are fleeing the market. Last week it was announced that one of the largest insurers is pulling out of Ohio — the great state of Ohio.” From the factcheck:

Trump decries that some insurance companies have announced they are leaving the Obamacare marketplace. But he ignores that many say they are exiting the business because of uncertainty created by the Trump administration, in particular whether it will continue to pay ‘cost-sharing reductions’ to insurance companies. These payments help reduce co-pays and deductibles for low-income patients on the exchanges. Without those subsidies, insurance companies have to foot more of the bill.

Kessler accidentally forgot to mention that the uncertainty created by the “cost-sharing reductions,” subsidies meant to entice insurance companies to participate in Obamacare’s fabricated exchanges, exists because they are unconstitutional. After all, the president can’t overturn a law. Trump has no duty to pay these subsidies; in fact, he probably has a duty not to. Congress never appropriated any funding for such payments. A federal court found that the Obama administration was acting unconstitutionally when it created them.

At the very least, this was a problem caused during the writing of the bill, not by Trump. Imagine what the sentinels of democracy at The Washington Post would be saying if Trump had ignored lower court rulings on the constitutionality of a travel ban?

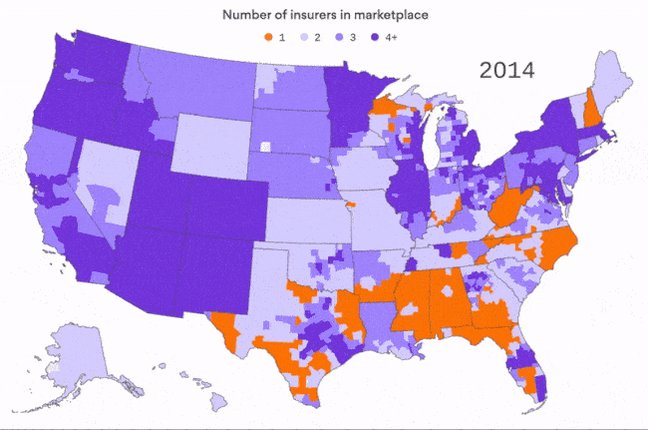

Whatever the case, despite Kessler’s non sequitur, Trump’s core contention that insurers are “fleeing” is well within the boundaries of a political truth. Kessler does nothing to debunk this claim. It is not mangled. Insurers were bolting before Trump became president. Here is a Kaiser Family Foundation map detailing insurance companies fleeing the Obamacare individual marketplace from 2014 to 2017.

If the word “fleeing” is worthy of three Pinocchios, you’d think someone would have written a comprehensive factcheck of the Democrats’ lie that 26 million people will “lose” their health insurance due to repeal bills. Six Pinocchios! Who knows? Maybe factcheckers will get around to pointing out that 16 million of the 24 million people Democrats claim will have their coverage snatched away are people who will choose not to buy it in the absence of a penalty. No doubt, factcheckers will point out that around six million or more of those 24 million who will supposedly have their coverage “taken” from them are people the CBO just assumes would have left Obamacare markets anyway. You know, baselines and all.

It is true that Obamacare repeal legislation — whatever the specifics happen to be — is going to be unpopular. Why wouldn’t it be? It’s not merely the revisionism practiced by many in the media in regards to Obamacare. If people are persistently told that the GOP is preparing to “slash” Medicaid by a bazillion dollars and “revoke” the insurance of 26 million people, the average voter has every reason to be concerned. And if there isn’t a single Republican lawmaker out there effectively slapping down these misleading claims, voters will be. Republicans certainly can’t rely on factcheckers.

David Harsanyi is a Senior Editor at The Federalist. Follow him on Twitter.

No comments:

Post a Comment